Would you like to download our mobile app from the App Store?

Download

Date of effect: 7.30 (AEDT) on 2 April 2019 to 30 June 2020

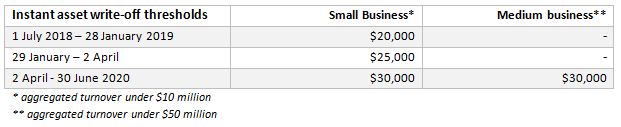

The threshold for the popular $20,000 instant asset write-off will increase to $30,000* from Budget night until 30 June 2020 when it will potentially return to its original $1,000 level on 1 July 2020. We say ‘potentially’ because the threshold has been at or above $20,000 since 12 May 2015.

The Government had previously announced an increase to the threshold for the instant asset write-off to $25,000 from 29 January 2019 but this measure was not legislated prior to the release of the Budget. The Government however intends to honour the announced rate increase.

In addition, the number of businesses that can access the instant asset write-off will increase. Currently, to qualify for the write-off, only businesses with an aggregated turnover under $10 million qualify. From Budget night, businesses with an aggregated turnover under $50 million will also be able to access the write-off.

Assets will need to be used or installed ready for use from Budget night until by 30 June 2020 to qualify for the higher threshold. Anything previously purchased does not qualify for the higher rate but may qualify for the $20,000 or $25,000 threshold. Similarly, anything purchased but not installed ready for use by 30 June 2020 will not qualify.

The instant asset write-off only applies to certain depreciable assets. There are some assets, like horticultural plants, capital works (building construction costs etc.), assets leased to another party on a depreciating asset lease, etc., that don’t qualify.

For assets costing $30,000 or more

For small businesses (aggregated turnover under $10m), assets costing $30,000 or more can be allocated to a pool and depreciated at a rate of 15% in the first year and 30% for each year thereafter. If the closing balance of the pool, adjusted for current year depreciation deductions (i.e., these are added back), is less than $30,000 at the end of the income year, then the remaining pool balance can be written off as well.

The ‘lock out’ laws for the simplified depreciation rules (these prevent small businesses from re-entering the simplified depreciation regime for five years if they opt-out) will continue to be suspended until 30 June 2020.

Pooling is not available for medium sized businesses which means that the normal depreciation rules based on the effective life of the asset will apply to assets that don’t qualify for an immediate deduction.

This initiative is subject to the passage of legislation so don’t go out on a spending spree just yet!

* $30,000 exclusive of GST for GST registered businesses. $30,000 inclusive of GST for businesses not registered for GST.

Date of effect: 1 July 2020

Division 7A captures situations where shareholders access company profits in the form of loans, payments or the forgiveness of debts. The rules are drafted broadly and have become more complex as amendments close perceived loopholes.

Division 7A treats certain events as triggering “deemed” dividends for tax purposes. Where a private company makes a payment or loan to a shareholder or associate, the amount may be treated as a dividend for tax purposes. Where a debt owed by a shareholder or associate to a private company is forgiven, these amounts may be subject to the same treatment.

Significant changes to the way Division 7A works were intended start taking effect from 1 July 2019. These reforms have now been pushed back to 1 July 2020.

These proposed reforms include:

The postponement is a welcome move to provide more time for the measures. In some cases, there will be quite a bit of work to be done to implement the reforms.

We will let affected clients know more when more information is released.

Date of effect: Vehicles acquired on or after 1 July 2019

For vehicles acquired on or after 1 July 2019, eligible primary producers and tourism operators will be able to apply for a refund of any luxury car tax paid, up to a maximum of $10,000.

Currently, primary producers and tourism operators may be eligible for a partial refund of the luxury car tax paid on eligible four wheel or all wheel drive cars, up to a maximum refund of $3,000. The eligibility criteria and types of vehicles eligible for the current partial refund will remain unchanged under the new refund arrangements.

Date of effect: Grants relating to flooding between 25 January 2019 and February 2019

The Government will ensure that qualifying grants paid to primary producers, small businesses and non-profit organisations affected by the North Queensland floods will be treated as non-assessable non-exempt income, which means that they should be tax-free.

Qualifying grants include Category C and Category D grants provided under the Disaster Recovery Funding Arrangements 2018, and grants provided under the On-Farm Restocking and Replanting Grants Program and the On-Farm Infrastructure Grants Program.

Date of effect: Payments relating to storm damage in October 2018

The Government will ensure that certain payments made to primary producers in the Fassifern Valley, Queensland who were affected by storm damage in October 2018 will be exempt from income tax.

$61m over three years has been provided to support Australian businesses to export Australian goods and services to overseas markets. $60m of the funding will go towards boosting reimbursement levels of eligible export marketing expenditure for small and medium enterprise exporters.

This article is for use of a general nature only and is not intended to be relied upon as, nor be substitute for, specific professional advice. No responsibility for loss occasioned to any persons or organisations acting on or refraining from action as a result of any information or material on our website will be accepted. Please ensure you contact us to discuss your particular circumstances and how the information provided applies to your situation.